Socrates spent decades as a teacher – or, as he liked to describe himself, a "midwife to the soul."

But then, an Athenian jury sentenced him to death for his ideas. When his friends and followers in attendance began weeping, Socrates spoke...

"What is this strange outcry? ... I have been told that a man should die in peace. Be quiet, then, and have patience."

Partly inspired by the story of Socrates' death, Zeno of Citium created the philosophy of Stoicism as a way of life. Its core principle: to find happiness, you must accept the present moment and the uncontrollable forces of nature... focus your efforts on things you can control... and not be consumed by desires.

In other words, you can't get through life without accepting the things you can't change during hard times.

Today, you need to be a "Market Stoic"...

With the market hitting new highs and valuations getting stretched, everyone wants to know how to dodge the big, looming crash. "When will it hit?" "How will I know when to get out?"

Unfortunately, no magic indicator can predict a crash. But don't worry. Even if the market corrects, we're likely not going to see a massive 40% fall – for one reason.

Let me explain...

You can't build your wealth in the market without accepting some volatility.

The market drops by 10% – the generally accepted measure of a "correction" – with surprising frequency. Even drops of 20% – "bear markets" – are common. It's going to happen.

Clearly, you want to avoid drops akin to the Great Depression, when the market collapsed 80% from its high and didn't reach a new one for almost 30 years... or the 2008-2009 financial crisis, when the market plummeted more than 50%.

But the 10% and 20% drops... they're just part of the game.

And believe me, if you've got, say, $500,000 in the market, watching $100,000 of your wealth evaporate feels devastating.

But it's not...

Most corrections are insignificant. If you set aside the major crises of the dot-com bust and the 2008-2009 financial crisis... over the last 12 corrections of 10% or greater, it has typically taken about five months to earn back losses. And sometimes the markets bounced back in as little as 32 days, like they did in 1997 or 1999.

But what about the true bear markets? Those big declines coincided with economic recessions.

Here's our tally of the past recessions along with the market pullbacks from peak to trough...

|

Recession Start

|

Recession End

|

Market Downturn

|

|---|---|---|

|

August 1929

|

March 1933

|

-86.0%

|

|

May 1937

|

June 1938

|

-54.0%

|

|

February 1945

|

October 1945

|

-29.6%

|

|

November 1948

|

October 1949

|

-20.6%

|

|

July 1953

|

May 1954

|

-14.8%

|

|

August 1957

|

April 1958

|

-20.7%

|

|

April 1960

|

February 1961

|

-13.9%

|

|

December 1969

|

November 1970

|

-36.1%

|

|

November 1973

|

March 1975

|

-48.2%

|

|

January 1980

|

November 1982

|

-27.1%*

|

|

July 1990

|

March 1991

|

-19.9%

|

|

March 2001

|

November 2001

|

-48.9%

|

|

December 2007

|

June 2009

|

-56.3%

|

|

Average

|

-36.6%

|

|

* Measures a single downturn from two twin recessions.

|

This picture looks grim. But it turns out, corrections just aren't as bad when they don't have a recession attached to them...

According to numbers compiled by Ben Carlson of Ritholtz Wealth Management, when the market drops without a recession, the average decline is only about 19.4%. And if you limit that to the modern era – 1970 onward – the average drops to 17.5%.

Just take a look at our tally of double-digit losses in the S&P 500 Index when we weren't in recession...

|

Time Frame

|

Market Downturn

|

|

1939-40

|

-31.9%

|

|

1941

|

-34.5%

|

|

1943

|

-13.1%

|

|

1947

|

-14.7%

|

|

1961-62

|

-26.4%

|

|

1966

|

-22.2%

|

|

1967-68

|

-10.1%

|

|

1971

|

-13.9%

|

|

1978

|

-13.6%

|

|

1983-84

|

-14.4%

|

|

1987

|

-33.5%

|

|

1998

|

-19.3%

|

|

2002

|

-14.7%

|

|

2010

|

-16.0%

|

|

2011

|

-19.4%

|

|

2015

|

-12.4%

|

The lesson here is simple... Ride out the recession-free declines in the markets like the bumps in the road that they are.

On that front, we need to check in on the economy... It's strong.

The latest quarter's real gross domestic product (GDP) growth checked in at 3.2%. Unemployment is low, only 4.1% last month. Job creation is strong... And industrial production is growing.

You can't, won't, and shouldn't try to time a 20% correction in the market with your retirement portfolio. It's going to happen. It's the price of playing the game.

And given the state of the economy, there's little reason to suspect a decline worse than that.

Eventually, whether it's in the next month or year or two, the market will turn on all of us. And we'll need to sit back and take it... with calmness.

That's not to say we do nothing. Like the Stoics, we're going to focus on the things we can change.

Follow a thoughtful asset-allocation plan... set reasonable goals... and limit your investing to quality businesses that compound capital over time.

Here's to our health, wealth, and a great retirement,

Dr. David Eifrig

Editor's note: If you've saved for retirement, Dave says you need to know about a unique provision of the latest tax-reform bill. Thanks to this change, investors could collect thousands of dollars over the coming weeks. And recently, he told his Retirement Millionaire readers how to get positioned for the biggest payouts... Click here to learn more.

Further Reading:

One key group of stocks can tell investors if the economy is slowing down. "It's an early warning sign for the stock market... like a canary in a coal mine," Steve writes. Learn more here.

"Keeping your wealth stored in a good, diversified mix of assets is the key to avoiding catastrophic losses," Dave writes. Read more about how to prepare for market pullbacks right here.

Recessions typically happen soon after stock market peaks. So if you have an indicator that can predict the next recession... then you have an indicator that can predict the next market peak. We have one indicator that does this – well in advance...

Market Notes

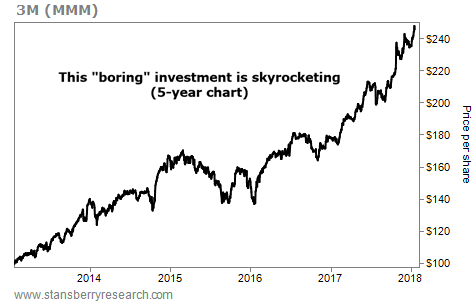

ANOTHER 'BORING' BUSINESS – WITH ATTRACTIVE GAINS

Today, one of our favorite investing strategies is paying off again...

Contrary to popular belief, you don't need to make risky bets to succeed in the stock market. Longtime readers know simple businesses often reward shareholders the most. These companies make steady profits on everyday goods like soda, pet food, and cleaning products. That's a great recipe for lucrative, long-term investments...

For proof, we look at manufacturing conglomerate 3M (MMM). This $145 billion giant makes "boring" household products like ACE bandages, Post-it notes, and Scotch tape. 3M has grown its bottom line consistently over the past several years... And it's passing those rewards on to its shareholders. The company has now raised its dividend for 58 years straight. Still, this isn't the type of stock you'll hear about at cocktail parties.

And that's OK with us... As you can see in the chart below, 3M shares are soaring to record highs. They've climbed 180% over the past five years... And they've risen 40% over the past year alone. Investing in tape and sticky notes may not be exciting, but it works...